Acknowledging that "the current system did not function well" the Chancellor announced proposed changes to the alcohol duty system in this week's budget which, subject to consultation, are expected to come into force in February 2023.

The new approach sees the proposed introduction of a standard method of taxation, taxed in proportion to ABV. The changes are intended to address public health concerns and address inconsistencies.

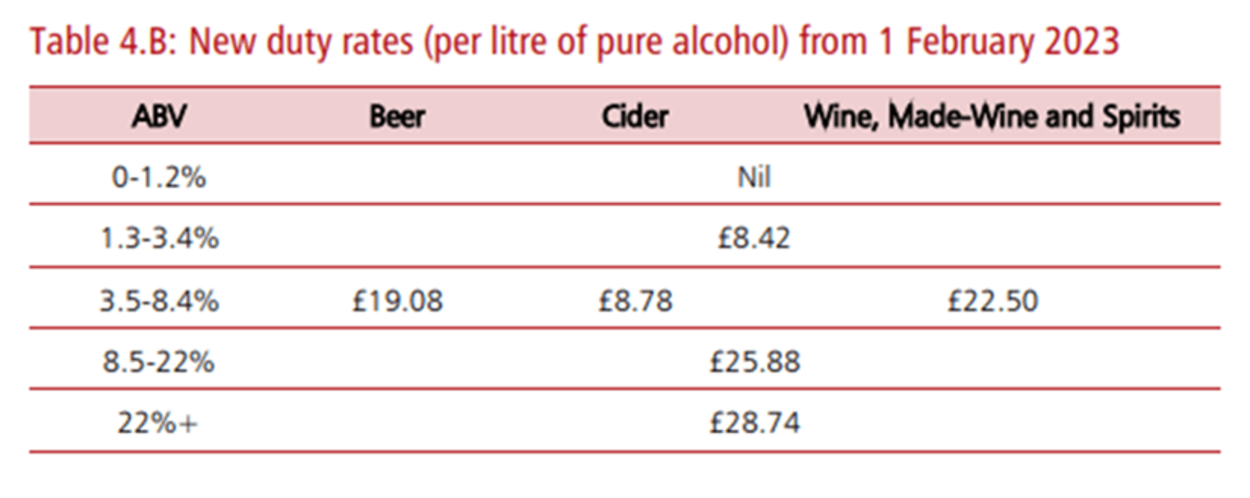

Statement of basic principles – "the stronger the drink the higher the rate"

1. All products should be taxed in direct proportion to their ABV.

2. Products with the same ABV should pay the same rate of tax.

3. The duty structure should be progressive, with rates increasing as the ABV increase.

How will these principles be implemented?

The government hopes to introduce a alcohol duty system that is simple, fair and consistent, which encourages innovation, supports public health and supports on-trade.

1. All products will be taxed by reference to litres of pure alcohol (ABV).

This replaces the three different approached which existed and applied depending on the product.

2. Standardisation of rates.

Noting that rates for ABV below 3.5% and above 8.5% will be the same regardless of the product.

These bands and rates are subject to consultation.

3. Draught Relief

Providing support to the on-trade, these new rates apply to draught products, not only to beer, but also to cider and made wines.

Qualifying products must have an ABV of less than 8.5%; be in large containers no less than 40L; and sold to connect to a dispensing system.

These rates, structure and criteria, as well as fraud prevention concerns and product diversion are open to consultation.

4. Small Producers Relief

This will apply to beer, cider, wine/ wine made products as well as spirit based products and is proposed to mirror the Small Brewers Relief (the government's response to the consultation on SBR is awaited). Qualifying business will be entitled to reduced rates on products with less than 8.5% ABV.

To qualify producers will need to produce less than the maximum threshold of pure alcohol per calendar year and it will be based on the previous calendar year's production with reference to the total hectares of pure alcohol (hLpa) and total production across all categories when considering the taper calculation. Tapering is welcomed as when the threshold is exceeded the benefit of SBR is lost completely.

It will not be possible to qualify if the product is made under licence (e.g., an existing beer brand) and products above an 8.5% ABV will count towards the production thresholds in order to prevent large producers qualifying for SBR in a new product category.

The thresholders, taper start point and maximum amount of reduction are all subject to the consultation.

5. Administration

The government is seeking a system which would enable producers to operate under one system: a single approval process allowing production of all alcohol types on multiple sites; an on-line system asking only questions relevant to the approval sought; and diversification need only be notified to HMRC and approvals updated, similarly expansion would only require notification and plan of the new site to be added to any existing approval.

This single alcohol approval would allow the production of alcohol as well as allow the producer to hold product made by themselves. If holding product elsewhere this would not involve duty payments.

Finally, a single duty return is proposed to cover all premises types and a standardisation of payment methods.

Our Food and Drink hub demonstrates our sector expertise and we are hosting our Food & Drink conference on 16 November.

Contributor

Partner